Grad PLUS Loans: The "Plus" They Don't Want You to See

3 min read

Family, let me ask you something.

When you hear the word "plus," what comes to mind? More. Better. A bonus. Something working in your favor.

So when the government calls it a Grad PLUS Loan, it sounds like a good thing, right?

It's not.

Real talk — the "plus" in Grad PLUS Loan just means more debt stacked on top of the debt you already have. And today, I'm going to break down exactly what these loans are, how they work, and why you should think twice — actually, three times — before signing on that dotted line.

Let's get to work.

What Is a Grad PLUS Loan?

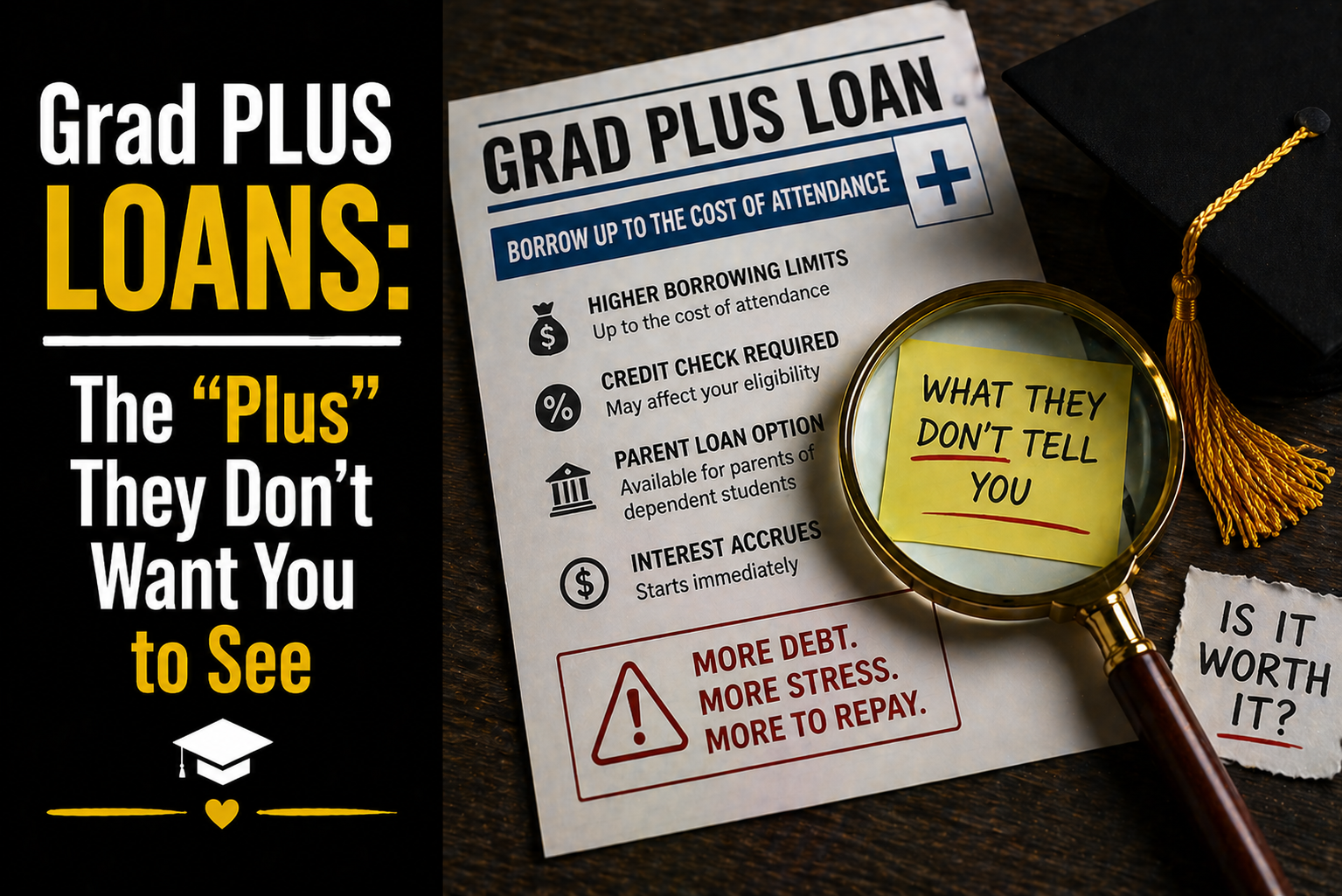

A Grad PLUS Loan is a federal loan offered to graduate and professional students to help cover the gap between what other financial aid covers and what school actually costs.

Here's the basic breakdown of how they work:

- You can borrow up to the full cost of attendance at your school

- Approval is based on your credit history (no adverse credit history allowed)

- There's a loan origination fee of 4.228% — meaning you're already in the hole before classes start

- The fixed interest rate is 9.08% — one of the highest rates in the federal loan system

- Interest starts accruing the moment the loan is disbursed — not after graduation

- These loans can be consolidated with other federal loans

So let's be clear: this is not free money. This is not a scholarship. This is debt — with a high interest rate and fees attached — that you will have to pay back.

What Does a Grad PLUS Loan Cover?

Grad PLUS Loans are designed to cover the costs that other financial aid doesn't. Most students turn to them after they've already maxed out their Direct Unsubsidized Loans — which cap at $20,500 per year for graduate students.

From there, a Grad PLUS Loan can cover things like:

- Tuition and fees

- Room and board

- Books and supplies

- Technology and equipment

- Other school-related expenses

Sounds helpful on the surface. But here's what they don't put in the brochure: by the time you graduate, the interest alone could add thousands — sometimes tens of thousands — of dollars to what you owe.

That's not a plus. That's a trap.

How Do You Apply for a Grad PLUS Loan?

To apply, you must:

- Be enrolled at least half-time in a graduate or professional degree program at a qualifying school

- Complete the FAFSA (Free Application for Federal Student Aid)

- Pass a credit check — no defaults, bankruptcies, or serious delinquencies on your record

- Meet general federal aid eligibility requirements (U.S. citizen, valid Social Security number, etc.)

- Complete loan entrance counseling if it's your first PLUS loan

- Sign a Master Promissory Note agreeing to the loan terms

Most schools direct you to apply through the Federal Student Aid website at studentaid.gov. Some have their own process. Either way, once you sign — you're on the hook.

Can Grad PLUS Loans Be Forgiven?

This is where a lot of people get their hopes up — and I don't want that to be you.

Yes, Grad PLUS Loans are technically eligible for:

- Income-Driven Repayment (IDR) plans — but these take 20 to 25 years to complete, and you have to meet strict conditions the entire time

- Public Service Loan Forgiveness (PSLF) — but this requires working for a qualifying nonprofit or government employer for 10 years straight

Here's the truth: loan forgiveness is not a plan. It's a maybe. It's a hope. And building your financial future on a maybe is not a strategy — it's a gamble.

And even if forgiveness does come through, you've spent years in a career path or income bracket that may not be what you actually wanted. That's a cost too.

Should You Apply for a Grad PLUS Loan?

I'm going to be straight with you, family: No.

I know that's not what some people want to hear. But I'd rather tell you the truth now than watch you spend the next 20 years paying for a decision you made in 20 minutes.

Here's the reality:

- That 9.08% interest rate is brutal. It compounds while you're in school, while you're in your grace period, and every single month after that.

- That 4.228% origination fee means if you borrow $20,000, you're already paying $845 before you attend a single class.

- Most graduate students already carry undergraduate debt on top of this.

- The job you're hoping to land after graduation is not guaranteed — and neither is the salary.

I've talked to doctors, lawyers, and dentists who are still paying off student loans from 15 and 20 years ago. Highly educated, high-earning professionals — still in bondage to debt they took on in their 20s.

That is not freedom. That is not the life God designed for you.

Real Alternatives to a Grad PLUS Loan

Here's the good news, family — you have options. Real ones. Let's talk about them.

1. Choose a School You Can Actually Afford

The name on your diploma matters less than you think. What matters is the knowledge, the network, and what you do with the degree. Research programs that fit your budget — including state schools, online programs, and institutions known for strong financial aid packages.

2. Apply for Graduate Scholarships

Scholarships aren't just for undergrads. There are thousands of graduate-level scholarships available — many of them go unclaimed every year because people don't apply. Use databases like Scholarship Owl or your school's financial aid office to find what you qualify for.

3. Look Into Graduate Assistantships

Many universities offer graduate assistantships — paid positions where you assist professors, conduct research, or teach undergraduate courses. In exchange, you often receive a tuition waiver plus a stipend. This is one of the most underutilized tools in grad school funding.

4. Ask Your Employer About Tuition Reimbursement

If you're working full-time and pursuing a degree in your field, your employer may cover part — or all — of your tuition. Many companies offer tuition reimbursement programs, especially if the degree directly benefits the business. Ask your HR department before you assume it's not available.

5. Still Fill Out the FAFSA

Even if you're not taking out loans, fill out the FAFSA. It opens the door to grants, work-study programs, and other aid you don't have to pay back. Don't leave free money on the table.

6. Cash Flow Your Education

This one takes discipline — but it's possible. Pay for school one semester at a time, out of pocket. Work while you study. Cut expenses. Pick up a side income. It may take longer, but you'll graduate with zero debt and a head start on building real wealth.

7. Consider Graduate Certificates

Depending on your goals, a full graduate degree may not be necessary. Graduate certificates are shorter, more affordable, and can still open doors in your field. They're worth exploring before committing to a two- or three-year program with a six-figure price tag.

The Bottom Line

Family, I know grad school feels like the next logical step. I know it feels like the responsible move. But taking on a Grad PLUS Loan with a 9.08% interest rate and a 4.228% origination fee — on top of debt you may already have — is not responsible. It's risky.

Here's what we covered today:

- A Grad PLUS Loan lets you borrow up to the full cost of attendance — but at a steep price

- Interest starts the moment the loan is disbursed, not after graduation

- Loan forgiveness is not a guaranteed plan

- There are real, practical alternatives that don't require you to go deeper into debt

Here's your move: Before you apply for any graduate loan, sit down and map out every alternative first. Scholarships. Assistantships. Employer reimbursement. Cash flowing. Exhaust every option before you sign your name to more debt.

Your future self will thank you.

Now I want to hear from you — are you considering grad school? What's your plan to fund it without going into debt? Drop it in the comments below. Let's figure this out together.

Keep building,

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

like what you’ve just read?

Make sure to share it with your tribe!

like what you’ve just read?

Make sure to share it with your tribe!