The Only Investing Guide You'll Need in 2026 (Start With Just $10)

3 min read

What if I told you that most people think financial freedom is about how much you make—but they're dead wrong?

Here's the truth: It's about building a future that pays you back. And in 2026, the game is changing. If you don't have a plan, you're going to get left behind while others build portfolios that pay them every single month without lifting a finger.

But here's the good news, family—you don't need thousands of dollars to start. You don't need a finance degree. You just need a strategy and the willingness to take that first step.

Today, I'm breaking down exactly how to calculate your freedom number, the mindset shifts you need for 2026, and the step-by-step blueprint to start investing—even if you only have $10 to your name.

Let's get to work.

🎬 Watch the Full Breakdown

Want to go deeper? I sat down with investing expert Courtney Hale to break this down step-by-step:

Prefer to read? Keep scrolling—I've got you covered.

What Is Your Freedom Number (And Why It Matters)?

Real talk—most people have no idea what they're actually working toward. They invest because someone told them to, but they've never asked the most important question: What's my number?

Your freedom number is the amount of money you need in your portfolio so you never have to trade time for money again. This is when your portfolio pays YOU every single year—whether you're working, traveling, or spending time with your grandkids.

Here's the simple math:

- Figure out how much you need to live comfortably per year (think about healthcare costs, housing, lifestyle)

- Divide that number by 0.05 (this assumes you'll live off 5% of your portfolio annually)

Example: If you need $100,000/year to live comfortably:

- $100,000 ÷ 0.05 = $2,000,000

That means a $2 million portfolio will pay you $100,000 every single year without touching your principal.

Now, before you panic at that number, hear me out. The goal isn't to save $2 million in cash—it's to invest consistently so compound interest does the heavy lifting. And if you're debt-free following my philosophy? That $100,000 goes a LOT further when you're not sending money to credit card companies every month.

"Most people think getting money means buying chains, cars, and designer clothes. But wealthy people? They're buying assets first." — Anthony O'Neal

The 2026 Mindset Shift: From Learning to Owning

2025 was the year of learning. You watched the videos. You followed the market. You saw things work.

2026 is the year you OWN it.

Here's what that means:

- You have a plan — not just good intentions

- You have an opportunity list — companies and ETFs you're ready to buy when dips happen

- You review your retirement accounts — understanding exactly what you're invested in

- You automate everything — so investing happens whether you remember or not

The biggest mistake I see beginners make? Waiting for the perfect time.

Listen, family—there is no perfect time. In 2025, we had three major market dips. The people who were ready? Some of them saw 70% returns on big names. The people who were "waiting to learn more"? They watched from the sidelines.

The dip is a bonus, not the strategy. You need to already be investing consistently. Then when opportunities come, you're ready to move.

How to Start Investing With Just $10 (Step-by-Step)

I know what some of you are thinking: "Anthony, I don't have thousands to invest. I'm still paying off debt."

I hear you. And here's what I need you to understand—the first habit of building wealth isn't how much money you have. It's taking the first step.

Step 1: Open a Brokerage Account (Tonight)

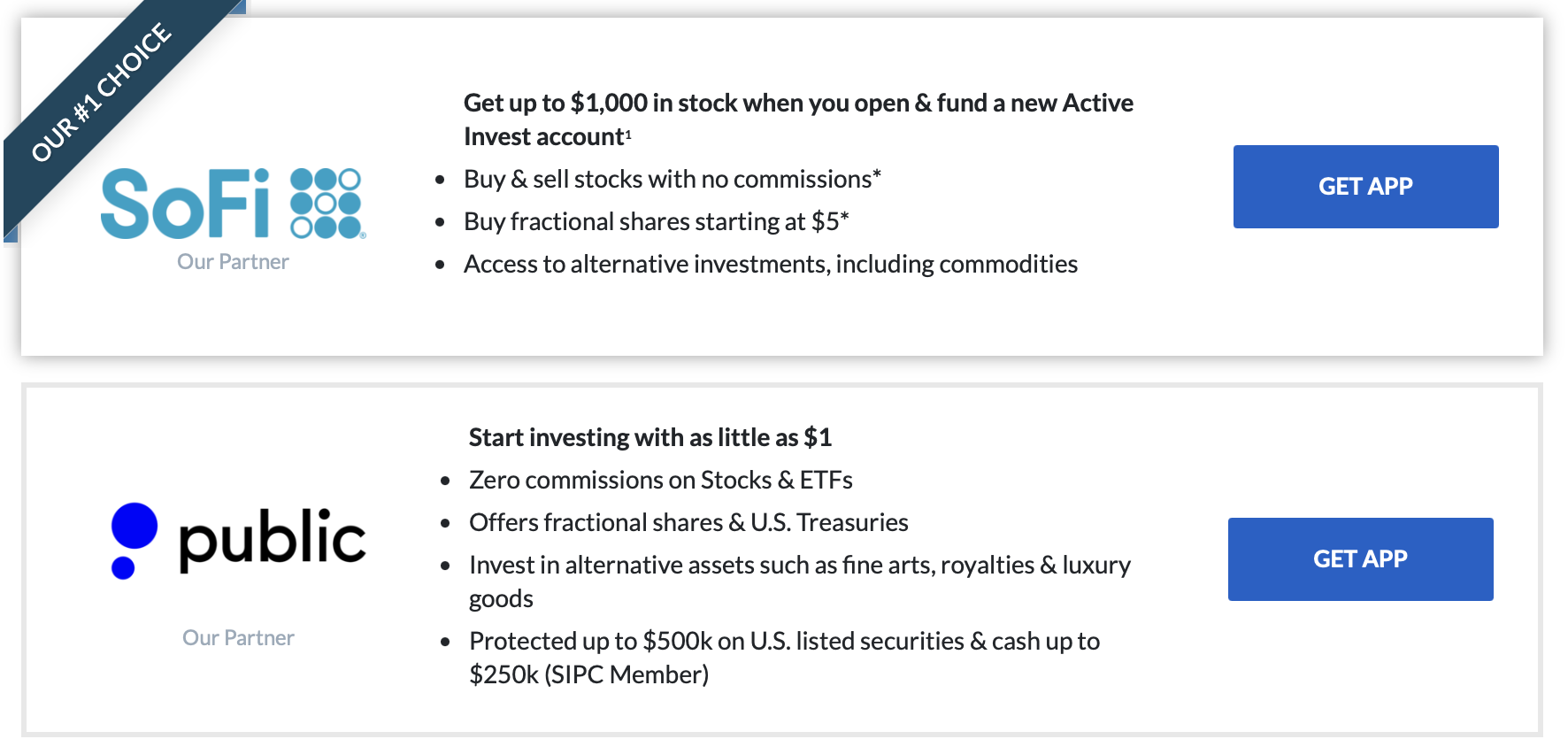

Don't overthink this. Pick a platform—SoFi, Public, Fidelity—and open an account. Most don't require any money upfront. You're just building the habit.

The IRS doesn't have problems getting their money because it's automated. Do what the IRS does—automate your investing.

👉 Ready to Open Your Account?

I've partnered with the top investing platforms to help you get started—many offer free stocks just for signing up. Compare your options and find the right fit for you.

Step 2: Set Up Automatic Transfers

Look at your monthly budget. How much can you comfortably move into your brokerage account every month? Even if it's $25 or $50—set it up to transfer automatically from your checking account.

Here's the key: 80-85% of that money should buy investments automatically. The other 15%? Let it sit there so when a dip comes, you're ready.

Step 3: Start With Index Funds (Not Individual Stocks)

Remember BlackBerry? They were the iPhone before the iPhone. If you had put all your money in BlackBerry stock, you'd be broke today.

That's why I recommend index funds and ETFs for beginners. You're buying a piece of hundreds of companies at once, spreading your risk.

The S&P 500 has averaged about 10% returns historically. Let's do the math:

- $100/month at 10% for 30 years = approximately $226,000

- $500/month at 10% for 30 years = approximately $1.1 million

That's the power of consistency and compound interest, family.

Step 4: Don't Panic When the Market Drops

Here's an analogy I love: Imagine you're holding a piece of paper. The market drops, and you crumple that paper in fear. Now try to flatten it back out—it's never quite the same.

When you panic-sell during a dip, you lock in your losses. The market has ALWAYS recovered over time. Your job is to stay the course.

The 50/50 Rule for Extra Money

Tax refund coming? Bonus at work? Side hustle income?

Here's my rule: 50% of any extra money goes toward investing or savings.

I know, I know—you've been telling yourself "I deserve this" for 15 years. You've done the vacation. You've bought the designer shoes. You've made the excuses.

It's time to flip the script.

- Get a $5,000 tax refund? $2,500 goes into your brokerage account.

- Get a $2,000 bonus? $1,000 goes toward your future.

This is how you turn active income into passive income. You're not just working for money anymore—you're working to build assets that will pay you and your children's children later.

What About Debt? Should I Invest While Paying It Off?

This is one of the most common questions I get, and here's my honest answer:

Yes—but strategically.

If you're drowning in high-interest debt (credit cards at 20%+), focus on knocking that out first using the debt snowball method. But here's what I don't want you to do: wait until you're 100% debt-free to start investing.

Why? Because time is your greatest asset. Every year you wait is a year of compound interest you'll never get back.

Here's my recommended order:

- Get your employer 401(k) match — that's free money, don't leave it on the table

- Build a $1,000 emergency fund — so you don't go back into debt

- Attack your debt aggressively — snowball method, smallest to largest

- Increase investments as debt decreases — aim for 15-25% of income eventually

The goal is progress, not perfection.

The Wealth Secret Nobody Talks About: Tithing

Now, I know this might ruffle some feathers, but I can't talk about building wealth without talking about this.

The first 10% of my income goes back to God. Before taxes, before bills, before anything.

"Anthony, how is that going to make me wealthy?"

Here's what I've learned: If I want God to trust me with more, I have to show Him I can be trusted with what I already have. Generosity isn't just about money—it's about your heart posture.

I've never seen God let a truly generous person go broke. Not once.

"Try God for 30 days. Tithe to your local church and watch what happens." — Anthony O'Neal

This isn't about math—the math won't make sense. It's about faith. And faith moves mountains that calculators can't measure.

Your 2026 Investing Action Plan

Let me make this cookie jar simple for you:

This Week:

- Calculate your freedom number (annual expenses ÷ 0.05)

- Open a brokerage account (even if you don't fund it yet)

- Set up automatic transfers (start with whatever you can afford)

This Month:

- Review your 401(k) — check those expense ratios and fund options

- Create your opportunity list — 3-5 companies or ETFs you'd buy on a dip

- Audit your budget — find an extra $50-100/month for investing

This Year:

- Aim for 15-25% of income going toward retirement and investments

- Build 3-6 months of expenses in a high-yield savings account

- Stay consistent — don't panic-sell, don't skip months

Conclusion

Look, family—this isn't about getting rich overnight. It's about building a future where your money works for you instead of you always working for money.

We covered a lot today:

- Your freedom number — the exact amount you need to never work again

- The 2026 mindset — owning your financial future, not just learning about it

- Starting with $10 — because the first step matters more than the first dollar

- The 50/50 rule — turning extra income into lasting wealth

- Tithing — the wealth secret that doesn't make sense on paper but changes everything

The truth is, you're not too far behind. You're not too broke. You're just one decision away from a new story.

Here's your move: Open that brokerage account tonight. Not tomorrow. Not next week. Tonight

Compare platforms and get started → anthonyoneal.com/invest

Then come back and tell me: What's YOUR freedom number? Drop it in the comments—let's build together.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

like what you’ve just read?

Make sure to share it with your tribe!

like what you’ve just read?

Make sure to share it with your tribe!